The Nuclear Renaissance

After decades of underinvestment, nuclear energy is experiencing a historic comeback. Governments, corporations, and investors worldwide are recognizing that nuclear power is essential for meeting climate goals while providing reliable baseload electricity.

Operating Reactors

About 438 nuclear reactors operate in 31 countries (~397 GWe), supplying approximately 9% of the world's electricity — and roughly a quarter of all low-carbon electricity globally.

Under Construction

Around 80 new nuclear reactors are being built worldwide, adding a combined ~76 GWe of capacity — concentrated in China, India, Russia, Turkey, and Egypt.

Planned Reactors

Around 110 power reactors (~107 GWe) are in advanced planning with approvals or funding in place, and a further ~290 GWe is proposed across all continents.

Demand by 2040

Annual reactor uranium requirements are projected to rise from ~69,000 tU today to more than double by 2040 in the World Nuclear Association's reference scenario, driven by new builds and reactor life extensions.

Supply Crisis

A Growing Supply Deficit

Current global uranium mine production covers only about 75% of reactor requirements. The deficit is being filled by depleting secondary sources — inventories that are rapidly running out.

Underinvestment Since 2011

Following the Fukushima incident, uranium prices collapsed and exploration spending dried up. A decade of underinvestment means very few new mines are ready to produce.

Long Development Timelines

It takes 10-15 years to bring a new uranium mine from discovery to production. Even with rising prices, new supply cannot come online quickly enough to meet surging demand.

Kazatomprom Constraints

The world's largest uranium producer, Kazatomprom, has repeatedly trimmed its output targets — including a cut to its 2026 production — citing sulfuric acid constraints and a deliberate "value over volume" strategy.

Geopolitical Risk

Russia and its allies control a significant portion of global uranium enrichment. Western utilities are actively seeking to diversify supply to politically stable jurisdictions like Canada.

Price Outlook

The Path to Triple-Digit Uranium

After collapsing below US$20/lb in the years following Fukushima, uranium has entered a structural bull market. The spot price has reclaimed the mid-US$80s, while the long-term contract market that actually funds new mines is signalling that triple-digit prices are coming.

Spot Price

Per lb U₃O₈, mid-2026 — up from below $20 at the post-Fukushima low.

Long-Term Price

The term price hit a 14-year high in late 2025 and continues to climb.

Already Triple-Digit

Share of 2025 long-term volumes contracted at prices of $100/lb or more.

Utility Modelling

Price level utilities are building into the ceilings of new long-term contracts.

Utilities are already preparing for triple-digit uranium — many of the long-term contracts being signed today are built around prices near US$120 per pound.

Reflecting commentary from Grant Isaac, President of Cameco — the world's largest publicly traded uranium producer. With roughly 116 million pounds placed under long-term contracts in 2025 against annual reactor consumption of about 190 million pounds, utilities face a large, uncovered supply gap that they are racing to lock in.

Where Analysts See Prices Going

Bank and analyst spot-price forecasts now cluster in the US$80–$150 range, while several specialist uranium investors argue that prices of US$150–$200 per pound are achievable once utilities are forced back into the spot market to cover their needs. The reasoning is consistent across the board: it takes higher, sustained prices to incentivise the new mine development required to close a structural supply deficit — and that incentive price keeps moving up.

Sources: Cameco; TradeTech/UxC long-term price indicators; analyst commentary as reported by Yahoo Finance / Oilprice (June 2026). Prices are indicative and subject to change.

Catalysts

What's Driving Demand

Four powerful, reinforcing trends are converging to drive structural growth in uranium demand.

Net Zero Commitments

Over 130 countries have committed to net-zero emissions. Nuclear is the only proven technology that can provide reliable, carbon-free baseload power at scale. What began as a 22-nation pledge at COP28 has grown to 38 countries committed to tripling nuclear capacity by 2050.

AI & Data Center Boom

The explosive growth of AI is driving unprecedented electricity demand. Microsoft, Google, and Amazon have all signed nuclear power agreements. Microsoft even partnered to restart Three Mile Island's Unit 1 reactor — underscoring how critical reliable, clean power has become.

Small Modular Reactors (SMRs)

Next-generation SMR technology is unlocking nuclear power for smaller grids, remote communities, and industrial applications. Canada is a global leader in SMR development, with projects advancing in Saskatchewan — right where Xcite operates.

Energy Security

The Russia-Ukraine conflict has fundamentally shifted global energy policy. Nations are prioritizing energy independence, and nuclear power from domestically sourced uranium has become a matter of national security.

Uranium 101

Education Center

A curated learning resource for investors — follow uranium's journey from the high-grade ore beneath the Athabasca Basin, through fuel fabrication, and into the reactors powering the clean-energy transition.

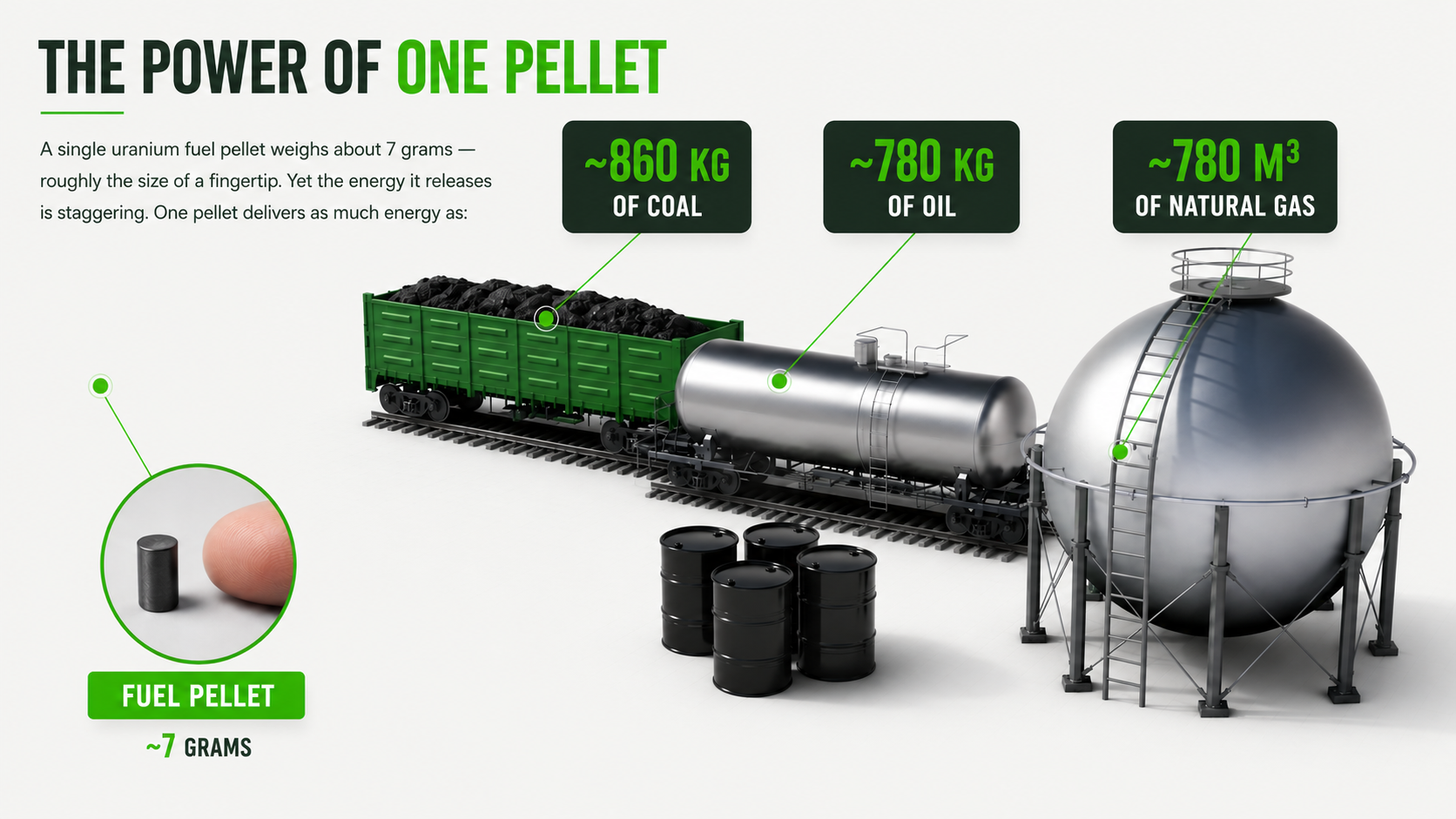

The Power of One Pellet

A single uranium fuel pellet weighs about 7 grams — roughly the size of a fingertip. Yet the energy it releases is staggering. One pellet delivers as much energy as:

Energy-equivalence figures are approximate and widely cited by the nuclear industry; actual output varies by reactor and enrichment.

Mining the Athabasca Basin

Saskatchewan's Athabasca Basin hosts the highest-grade uranium deposits on Earth. See how world-class operations like Cameco's Cigar Lake extract uranium safely from these remarkable orebodies.

Mining in the Athabasca Basin

Cameco's Cigar Lake Operation

How Uranium Becomes Nuclear Fuel

Mined uranium is milled into yellowcake, converted, enriched, and finally pressed into ceramic fuel pellets that are sealed into fuel rods. These videos walk through each step of the fuel cycle.

How Uranium Is Made Into Nuclear Fuel

The Nuclear Fuel Cycle Explained

How a Nuclear Reactor Works

Inside a reactor, the controlled fission of uranium atoms generates heat that produces steam to spin turbines — delivering reliable, carbon-free baseload electricity around the clock.

Featured How a Nuclear Reactor Works — A Visual Walkthrough

Nuclear Power Plant Fundamentals

From Fission to Electricity

Trusted Resources

Go deeper with these independent, industry-standard references on nuclear energy and the global reactor fleet.

Nuclear Essentials

World Nuclear Association — plain-language answers to the most common questions about nuclear energy.

World Reactor Database

World Nuclear Association — a live summary of operating, under-construction, and planned reactors worldwide.

How a Nuclear Reactor Works

Canadian Nuclear Association — a Canadian perspective on reactors and Small Modular Reactors (SMRs).

World Nuclear Association

The global industry organization — comprehensive data, country profiles, and analysis of the nuclear sector.

World-Class Location

The Athabasca Basin Advantage

Saskatchewan's Athabasca Basin is recognized globally as the premier uranium district — and it's where Xcite Uranium operates.

Global Supply

The Athabasca Basin supplies approximately 20% of global uranium production.

Higher Grade

Athabasca Basin deposits can be 10 to 100 times the grade of deposits elsewhere in the world.

Fraser Institute Rank

Saskatchewan ranks as the 3rd most attractive jurisdiction for mining investment globally (Fraser Institute 2026 survey).

lbs Historic Production

The Beaverlodge camp produced over 70 million lbs of uranium between 1950 and 1982.

Why Saskatchewan?

Explore the Xcite Uranium Opportunity

Five properties. Proven uranium district. Strong treasury. The right team at the right time.